Tutorial: Basics classifiers#

In this lab we will get more comfortable configuring various classifiers in R.

Goals:#

Learn to use the

glmfunction for logistic regressionLearn to use the

ldaandqdafunctions for doing discriminant analysis

This tutorial draws from the practice sets at the end of Chapter 4 in James, G., Witten, D., Hastie, T., & Tibshirani, R. (2013). “An introduction to statistical learning: with applications in r.”

Logistic regression with glm#

For the first part of the lab we will use the generalized linear model (glm) function to perform logistic regression. GLM is a way of formalizing all forms of linear models when the underlying statistical distribution is part of the exponential family. The linear regression models we have discussed so far in this class are a type of GLM, and logistic regression also falls under the GLM umbrella.

Predicting the stock market#

For the logistic regression exercises, we will use the S&P stock market data included with the ISLR library.

This dataset contains daily observations (n=1250) for the S&P 500 index between 2001 & 2005. The variables in this data set include:

Year: The year that the observation was recorded

Lag1: Percentage return for previous day

Lag2: Percentage return for 2 days previous

Lag3: Percentage return for 3 days previous

Lag4: Percentage return for 4 days previous

Lag5: Percentage return for 5 days previous

Volume: Volume of shares traded (number of daily shares traded in billions)

Today: Percentage return for today

Direction: A factor with levels Down and Up indicating whether the market had a positive or negative return on a given day

Remember that logistic regression, and classification more generally, is about working with categorical output variables. Guess which of the variables above is the one we’ll be predicting!

# Install the ISLR package (if you haven't yet)

install.packages("ISLR")

# Load the library

library(ISLR)

library(ggplot2)

# Uncomment the line below if you want to learn more about the dataset

#help(Smarket)

# Let's take a look at the distribution of our variables

summary(Smarket)

Installing package into ‘/usr/local/lib/R/site-library’

(as ‘lib’ is unspecified)

Year Lag1 Lag2 Lag3

Min. :2001 Min. :-4.922000 Min. :-4.922000 Min. :-4.922000

1st Qu.:2002 1st Qu.:-0.639500 1st Qu.:-0.639500 1st Qu.:-0.640000

Median :2003 Median : 0.039000 Median : 0.039000 Median : 0.038500

Mean :2003 Mean : 0.003834 Mean : 0.003919 Mean : 0.001716

3rd Qu.:2004 3rd Qu.: 0.596750 3rd Qu.: 0.596750 3rd Qu.: 0.596750

Max. :2005 Max. : 5.733000 Max. : 5.733000 Max. : 5.733000

Lag4 Lag5 Volume Today

Min. :-4.922000 Min. :-4.92200 Min. :0.3561 Min. :-4.922000

1st Qu.:-0.640000 1st Qu.:-0.64000 1st Qu.:1.2574 1st Qu.:-0.639500

Median : 0.038500 Median : 0.03850 Median :1.4229 Median : 0.038500

Mean : 0.001636 Mean : 0.00561 Mean :1.4783 Mean : 0.003138

3rd Qu.: 0.596750 3rd Qu.: 0.59700 3rd Qu.:1.6417 3rd Qu.: 0.596750

Max. : 5.733000 Max. : 5.73300 Max. :3.1525 Max. : 5.733000

Direction

Down:602

Up :648

# Next let's quantify all pairwise correlations as a first glimpse at the relationships among the variables

cxy = cor(Smarket)

Error in cor(Smarket): 'x' must be numeric

Traceback:

1. cor(Smarket)

2. stop("'x' must be numeric")

The code above returns an error - this is because calculating the correlations requires numeric variables, but the Direction variable is categorical.

# Look at the column for Direction

head(Smarket$Direction)

- Up

- Up

- Down

- Up

- Up

- Up

Levels:

- 'Down'

- 'Up'

# In order to see the correlation let's remove the Direction variable

cxy = cor(Smarket[,-which(colnames(Smarket)=="Direction")])

cxy

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | |

|---|---|---|---|---|---|---|---|---|

| Year | 1.00000000 | 0.029699649 | 0.030596422 | 0.033194581 | 0.035688718 | 0.029787995 | 0.53900647 | 0.030095229 |

| Lag1 | 0.02969965 | 1.000000000 | -0.026294328 | -0.010803402 | -0.002985911 | -0.005674606 | 0.04090991 | -0.026155045 |

| Lag2 | 0.03059642 | -0.026294328 | 1.000000000 | -0.025896670 | -0.010853533 | -0.003557949 | -0.04338321 | -0.010250033 |

| Lag3 | 0.03319458 | -0.010803402 | -0.025896670 | 1.000000000 | -0.024051036 | -0.018808338 | -0.04182369 | -0.002447647 |

| Lag4 | 0.03568872 | -0.002985911 | -0.010853533 | -0.024051036 | 1.000000000 | -0.027083641 | -0.04841425 | -0.006899527 |

| Lag5 | 0.02978799 | -0.005674606 | -0.003557949 | -0.018808338 | -0.027083641 | 1.000000000 | -0.02200231 | -0.034860083 |

| Volume | 0.53900647 | 0.040909908 | -0.043383215 | -0.041823686 | -0.048414246 | -0.022002315 | 1.00000000 | 0.014591823 |

| Today | 0.03009523 | -0.026155045 | -0.010250033 | -0.002447647 | -0.006899527 | -0.034860083 | 0.01459182 | 1.000000000 |

This gives us a sense of the relationship between the variables. While Volume and Year appear to be correlated (r=0.539) the rest of the variables appear to be weakly correlated at best.

So now, let’s use the built-in glm function to estimate the following model. $\( y_{direction} = \beta_0 + \beta_1 x_{lag1} + \beta_2 x_{lag2} + \beta_3 x_{lag3} +\\ \beta_4 x_{lag4} + \beta_5 x_{lag5} + \beta_{6} x_{Volume} + \epsilon \)$

This model tries to predict whether the stock market will end higher or lower on one day given the percent returns on the previous 5 days and the overall volume of shares traded.

For this analysis we need to define how \(Y\) (Direction) is distributed. For logistic regression we say that \(Y\) is binomially distributed (i.e., it arises from a binomial distribution).

# Run the GLM

glm.fit=glm(Direction~Lag1+Lag2+Lag3+Lag4+Lag5+Volume, data=Smarket, family=binomial) # logistic regression

# Summarize

summary(glm.fit)

Call:

glm(formula = Direction ~ Lag1 + Lag2 + Lag3 + Lag4 + Lag5 +

Volume, family = binomial, data = Smarket)

Deviance Residuals:

Min 1Q Median 3Q Max

-1.446 -1.203 1.065 1.145 1.326

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -0.126000 0.240736 -0.523 0.601

Lag1 -0.073074 0.050167 -1.457 0.145

Lag2 -0.042301 0.050086 -0.845 0.398

Lag3 0.011085 0.049939 0.222 0.824

Lag4 0.009359 0.049974 0.187 0.851

Lag5 0.010313 0.049511 0.208 0.835

Volume 0.135441 0.158360 0.855 0.392

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 1731.2 on 1249 degrees of freedom

Residual deviance: 1727.6 on 1243 degrees of freedom

AIC: 1741.6

Number of Fisher Scoring iterations: 3

As you can see, if we accept an \(\alpha = 0.05\) (i.e., p must be less than 0.05 for the effect to be statistically significant), then it doesn’t appear that the previous day’s performance or overall trading volume predicts whether the market ends up or down on a given day.

Let’s take a closer look at the model fits themselves.

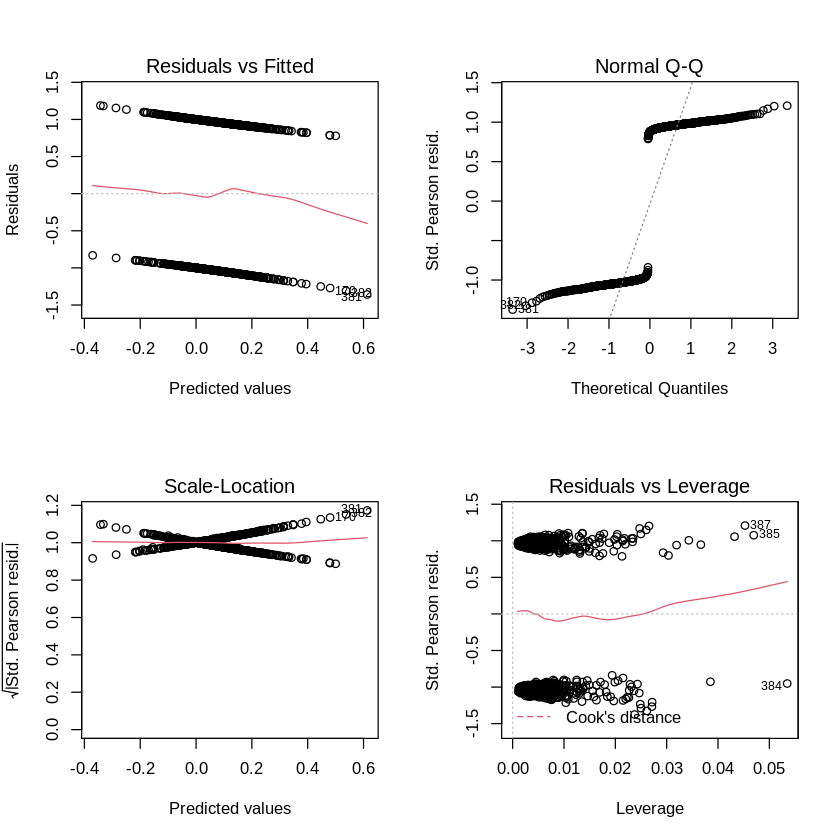

# Plot the model fit evaluation images

par(mfrow=c(2,2))

plot(glm.fit)

It appears that there are some high leverage points. But clearly, most of the other model fit evaluations that we used for linear regression don’t work for the logistic family.

We can also test the quality of the model fit itself. How do we do that? Use prediction.

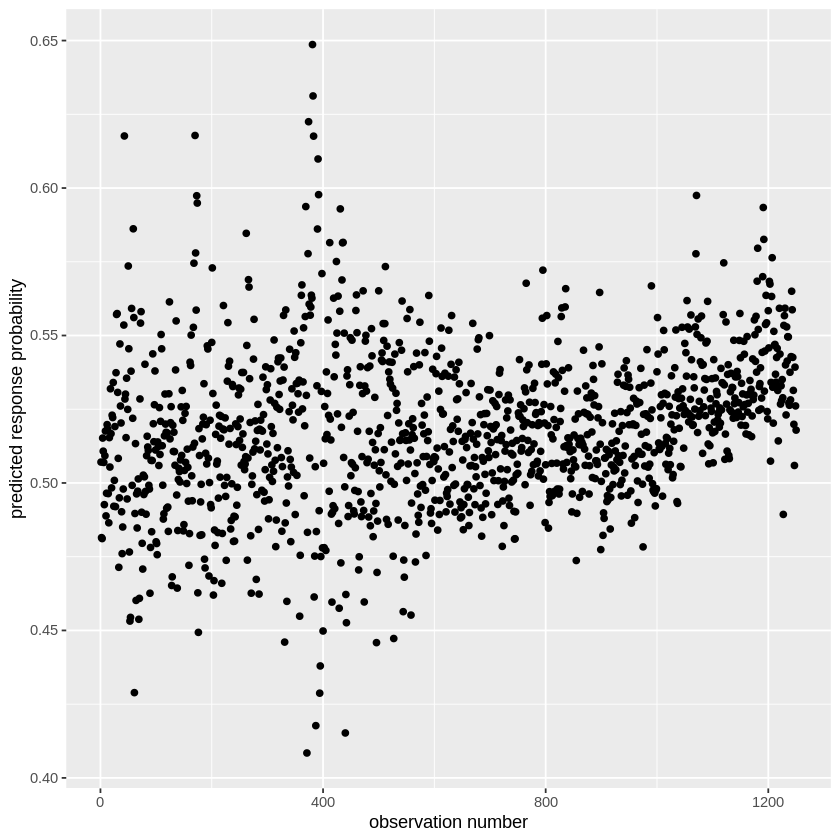

# See how well the model captured the training set

glm_prob_df = data.frame(predict(glm.fit, type = "response"))

colnames(glm_prob_df) = c('predicted_prob')

num_observations = nrow(glm_prob_df)

glm_prob_df$index = seq(1, num_observations) #get the observation number for plotting; ggplot does not infer this

# Setting type="response" tells R to output prob. from P(Y=1,X) for all values of X

# "If no data set is supplied to the predict() function, then the probabilities

# are computed for the training data that was used to fit the logistic regression model."

ggplot(glm_prob_df, aes(index, predicted_prob)) + geom_point() + xlab('observation number') + ylab('predicted response probability')

What we are showing here are the predicted Y values for our full model. Notice that they are not binary. Why? Because we are estimating Y as a sigmoid function, as we talked about during the lecture. Thus we aren’t predicting the direction, but the probability of the direction being “Up”. We know that these are the probabilities that the Stock Market will go up rather than down because we can check how R categorized the Direction variable using contrasts().

contrasts(Smarket$Direction)

| Up | |

|---|---|

| Down | 0 |

| Up | 1 |

Thus, if you want to make a binary prediction (i.e., did the market go up or down?), you need to set a threshold for the estimated outcome probability and binarize the result according to that threshold. Let’s try that.

threshold = 0.50 #binarizing threshold

# First make a list of "Downs"

glm_prob_df$predicted_binary=rep("Down",num_observations)

# Then use the probability output to label the up days. Let's use a threshold of 50% probability.

glm_prob_df$predicted_binary[glm_prob_df$predicted_prob>threshold]="Up" #find the rows that have prob > threshold and cast as 'up'

# Now let's look at the prediction accuracy

confusion_df = data.frame(glm_prob_df$predicted_binary, Smarket$Direction)

colnames(confusion_df) = c('predicted', 'actual')

table(confusion_df)

actual

predicted Down Up

Down 145 141

Up 457 507

This table is sometimes call the confusion matrix. The diagonal values (top left and bottom right) are the frequency of the correct predictions and the off diagonal (top right and bottom left) are the errors. We can estimate the overall accuracy by either summing the diagonal values and dividing by \(n\), the total number of observations, (i.e., (145+507)/1250) or more directly by seeing the average number of times the predicted value matched the observed.

Side note: you can create nicely formatted confusion matrices using the caret package and the fourfoldplot command, though I find the simple table easier to interpret.

# We can calculate the prediction accuracy by counting the number of times our

# prediction vector matched the real data and taking the average

print(paste("Accuracy:",mean(confusion_df$predicted == confusion_df$actual)))

[1] "Accuracy: 0.5216"

This means that we are correct ~52% of the time in estimating whether the market will end up or down on a given day. At first glance this might not seem that bad (it’s better than chance, 50%). However, remember, this is the error on the training data. So the actual performance of this model at predicting the stock market in the future (i.e., test accuracy) may be lower.

Let’s try a case where we try to predict the market performance in 2005, using the pre-2005 data.

# Let's isolate the years before 2005 to use as a training set to predict market change in 2005

# First create an index vector to find the entries corresponding to years < 2005

train_idx=(Smarket$Year<2005)

# Can now make a whole new Smarket dataset just for 2005 (it's the last year, so anything not train is 2005)

Smarket.2005_test = Smarket[!train_idx,] #find rows that do not (! = not) occupy the training data indices

dim(Smarket.2005_test) #get dimensions of the test data

# Now let's extract the Direction for just 2005

Direction.2005_test=Smarket.2005_test$Direction

- 252

- 9

For the sake of simplicity, let’s only use performance from the previous two days to predict the current stock market peformance. In other words, we’ll use this model: $\( y_{direction} = \beta_0 + \beta_1 x_{lag1} + \beta_2 x_{lag2} + \epsilon \)$

# Train the logistic model, but use only the subset of the data from pre-2005 (i.e., training data)

glm.fit=glm(Direction~Lag1+Lag2, data=Smarket, family=binomial, subset=train_idx) #give the training indices to the glm function

# Predict the 2005 performance from the model trained on the pre-2005 data

glm.probs=predict(glm.fit, Smarket.2005_test, type="response")

glm.pred=rep("Down",nrow(Smarket.2005_test)) # There are only 252 observations in the test set.

glm.pred[glm.probs>0.5]="Up" #binarize the result

confusion_df = data.frame(glm.pred, Direction.2005_test) #create confusion df

colnames(confusion_df) = c('predicted', 'actual')

# Show the confusion matrix

table(confusion_df)

actual

predicted Down Up

Down 35 35

Up 76 106

# Now let's look at the overall test accuracy

print(paste("Accuracy:",mean(confusion_df$predicted == confusion_df$actual)))

[1] "Accuracy: 0.55952380952381"

So this isn’t too bad. We can predict slightly above chance the 2005 performance from a model trained on the previous years.

LDA#

Let’s now move on to using LDA. The lda function is built into the MASS library that we have used previously. We’ll use that one here (although there are other LDA libraries that you can install if you’d like).

First let’s replicate our prediction problem using the stock market data.

library(MASS)

# LDA syntax is just like for linear regression fitting

# Let's conduct LDA on the training subset now

lda.fit = lda(Direction~Lag1+Lag2, data=Smarket, subset=train_idx)

lda.fit # The summary() function gives you something different

plot(lda.fit)

Call:

lda(Direction ~ Lag1 + Lag2, data = Smarket, subset = train_idx)

Prior probabilities of groups:

Down Up

0.491984 0.508016

Group means:

Lag1 Lag2

Down 0.04279022 0.03389409

Up -0.03954635 -0.03132544

Coefficients of linear discriminants:

LD1

Lag1 -0.6420190

Lag2 -0.5135293

This indicates that 49.2% of the training observations correspond to days during which the market went down.

The coefficients of linear discriminants indicate the distance of each value from the discrimination boundary.

If \(w_1*x_{Lag1} - w_2*x_{Lag2}\) is positive, then the classifier predicts the market will increase

If \(w_1*x_{Lag1} - w_2*x_{Lag2}\) is negative, then the classifier predicts the market will decrease

Now let’s use LDA to predict the market values in 2005. LDA determines the group assignment by assigning above and below the 50% (0.5) posterior probabiltiy. In otherwords if the posterior probability is >=0.5, then it assigns one value, otherwise it assigns the other.

# Predict from your LDA coefficients

lda.pred = predict(lda.fit, Smarket.2005_test)

# We next extract the output of the prediction

lda.class = lda.pred$class

table(lda.class, Direction.2005_test)

print(paste("Accuracy:",mean(lda.class==Direction.2005_test)))

Direction.2005_test

lda.class Down Up

Down 35 35

Up 76 106

[1] "Accuracy: 0.55952380952381"

So we now see that the LDA is performing just as well as the logistic regression at ~56% test set accuracy.

Another way to evaluate the LDA is by looking at the posterior probability from the model. This is analogous (although not identical) to \(\hat{y}\), our estimate of the probability of being “Up”, in the logistic regression example.

head(lda.pred$posterior)

| Down | Up | |

|---|---|---|

| 999 | 0.4901792 | 0.5098208 |

| 1000 | 0.4792185 | 0.5207815 |

| 1001 | 0.4668185 | 0.5331815 |

| 1002 | 0.4740011 | 0.5259989 |

| 1003 | 0.4927877 | 0.5072123 |

| 1004 | 0.4938562 | 0.5061438 |

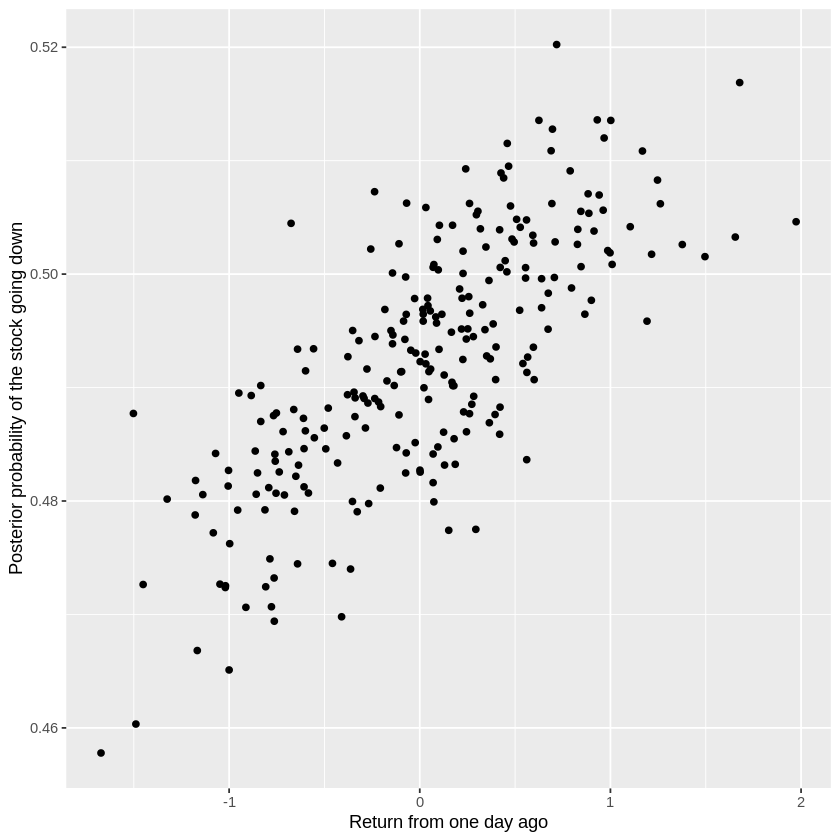

Sometimes it is more informative to look at the relationship between a predictor variable and the posterior, rather than a predictor variable and the predicted classification. It helps you distinguish between, for example, observations that are very likely to be “Down” and observations that are only somewhat likely to be “Down”.

# Show the relationship between the Lag 1 variable

# and the posterior probability from LDA

lag1_posterior_df = data.frame(Smarket.2005_test$Lag1, lda.pred$posterior[,1])

colnames(lag1_posterior_df) = c('lag1_return', 'down_posterior_prob')

ggplot(data=lag1_posterior_df, aes(lag1_return, down_posterior_prob)) + geom_point() + xlab('Return from one day ago') + ylab('Posterior probability of the stock going down')

#getting the lag 1 percentage return & the posterior prob. of the stock going down

QDA#

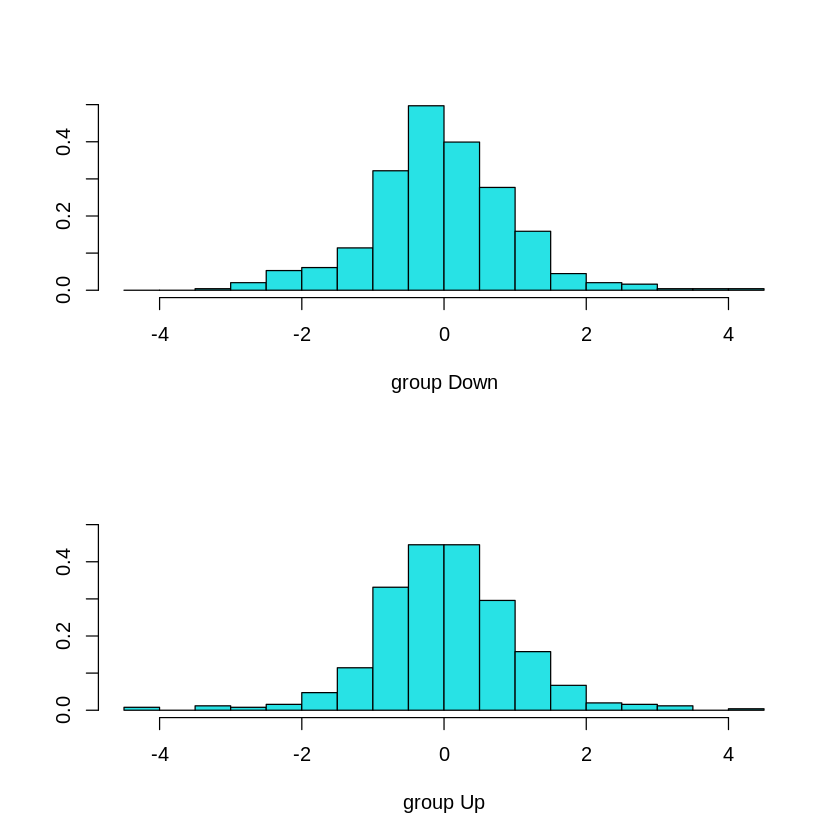

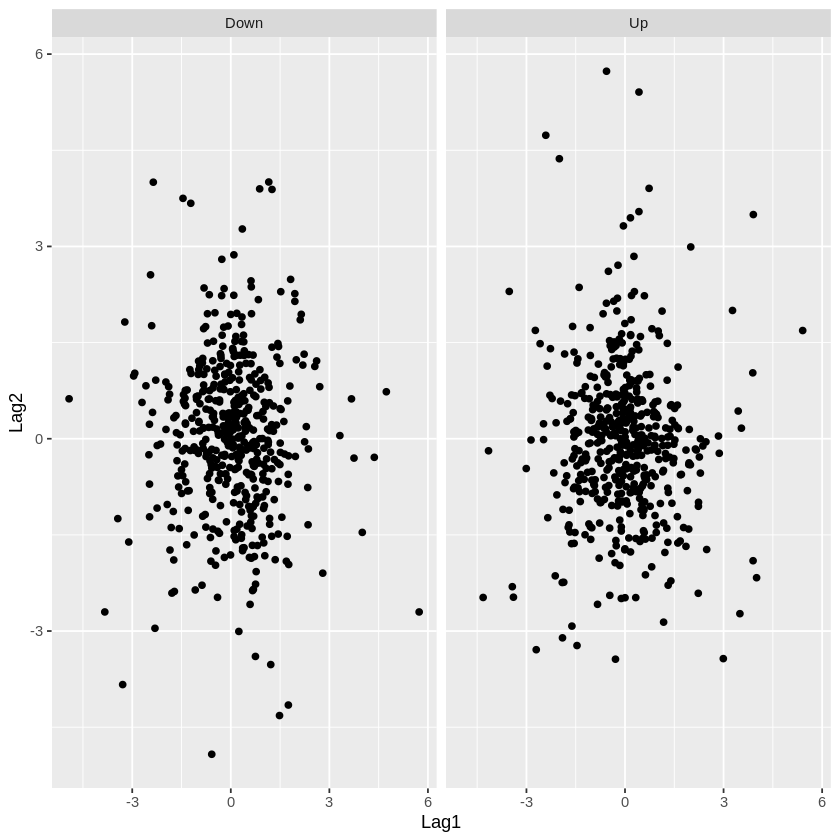

Remember that QDA is a special case of LDA where you do not assume that the underlying distributions have equal variances. So let’s use QDA for the same problem we have been working on so far. First off, let’s check how the distributions of Lag1 and Lag2 look in the case of Direction="Up" and Direction="Down". This will help us think about whether QDA might be a better tool than LDA for our question.

ggplot(Smarket[train_idx,],aes(x=Lag1,y=Lag2)) + geom_point() + facet_grid(.~Direction)

print(paste("Covariance of Lag1, Lag2 for Up observations:",

cov(Smarket$Lag1[train_idx][which(Smarket$Direction[train_idx]=="Up")],Smarket$Lag2[train_idx][which(Smarket$Direction[train_idx]=="Up")])))

print(paste("Covariance of Lag1, Lag2 for Down observations:",

cov(Smarket$Lag1[train_idx][which(Smarket$Direction[train_idx]=="Down")],Smarket$Lag2[train_idx][which(Smarket$Direction[train_idx]=="Down")])))

[1] "Covariance of Lag1, Lag2 for Up observations: -0.0278734923872115"

[1] "Covariance of Lag1, Lag2 for Down observations: -0.0392480610374496"

There is definitely a fair amount of overlap in these distribution (which helps us understand why all our classifiers have low accuracy: the means of the two distributions, \(\mu_{1}\) and \(\mu_{2}\), are very close). However, the main advantage of QDA is allowing for differences in variance of the two distributions. Looking at the clusters and statistics above, the “Down” observations might have a slightly more negative covariance than the “Up” observations. Note that since there are only two predictor variables here, Lag1 and Lag2, covariance is a single value instead of a matrix (like \(\Sigma_k\) described in Chapter 4 of the James et al., 2013 text).

Now that there’s a possibility QDA could help, let’s try it:

# QDA is also part of the MASS library

qda.fit = qda(Direction~Lag1+Lag2, data=Smarket, subset=train_idx)

qda.fit

# Same basic predictions as LDA, just assuming that each distribution has its own variance.

# But we work with coefficients the same way.

qda.class=predict(qda.fit, Smarket.2005_test)$class

table(qda.class, Direction.2005_test)

print(paste("Accuracy:",mean(qda.class==Direction.2005_test)))

Call:

qda(Direction ~ Lag1 + Lag2, data = Smarket, subset = train_idx)

Prior probabilities of groups:

Down Up

0.491984 0.508016

Group means:

Lag1 Lag2

Down 0.04279022 0.03389409

Up -0.03954635 -0.03132544

Direction.2005_test

qda.class Down Up

Down 30 20

Up 81 121

[1] "Accuracy: 0.599206349206349"

Notice that QDA is doing slightly better than LDA, with a test accuracy of 60%.

Notebook authored by Ven Popov and edited by Krista Bond, Charles Wu, Patience Stevens, and Amy Sentis.